Pennsylvania state capitol building

John Greim/LightRocket | Getty Images

It is not an easy time to be the treasurer of Pennsylvania.

Joseph Torsella, a Democrat elected treasurer in 2016, has to cope with a simple fact of life: age. His politically important swing state has the sixth largest economy in the nation — but it also has an aging population, 18.2% over 65, compared with a national average of 16%.

“Some of these numbers suggest a kind of torpor,” Torsella says.

In an era when most political innovation is coming at the state level, Torsella is emerging as a leader, with a host of initiatives — from a pugilistic lawsuit against Wall Street to a package of cutting-edge programs aimed at getting Pennsylvanians to save more — driven by behavioral finance insights. This includes investing $100 for every baby born or adopted in the state on or after Jan. 1, 2019, if it is used for higher education. (As part of a demonstration project, babies born in 2018 in six counties may also be eligible but must claim their grant by the child’s first birthday.)

Pennsylvania‘s $34 billion budget is balanced this year, but if Torsella doesn’t succeed, it might not be for long.

Torsella has had to cope with a pension fund crisis, winning praise for a 2017 reform and follow-on measures. But Pennsylvania still has major unfunded pension liabilities, ranking ninth on the Pew’s list of state unfunded pension liabilities with an assets-to-liabilities ratio of just 55% (80% is considered healthy). That is one reason why the state is ranked No. 28 on CNBC’s 2019 Top States for Business ranking, released Wednesday.

Torsella recently became lead plaintiff in a class-action case in which public institutional investors are suing 15 banks and trading desks for fixing prices on Fannie Mae/Freddie Mac bonds. Pennsylvania transacted $63 billion in these bonds between 2009 and 2014, according to Torsella’s office. A few percentage points made a big difference.

A looming pension crisis

In an era where Social Security doesn’t deliver nearly enough for most people to live on, an aging population means not only big problems in the pension system but big draws on state resources. A growing number of Pennsylvanians will be hitting their retirement years without enough private savings in 401(k)s and IRAs — which means they’ll be drawing on Medicaid and other state-funded programs for help.

In 2015, people without enough retirement savings cost Pennsylvania $700 million a year. By 2030 it’ll be $1.1 billion a year, totaling a cumulative $14.3 billion from 2015 to 2030, according to a report from the Pennsylvania treasurer’s office.

Without strong economic growth from other sources, the state’s economy won’t be able to sustain those needs. And other sources of economic growth haven’t appeared — the Rust Belt giant has low immigration, flat population growth, below-average job gains, and it’s No.1 in student debt, to boot.

Faced with the bleak scenario, Torsella is turning to surprising initiatives to make a difference. Call it the power of small numbers. He figures if he can get Pennsylvanians saving, he can make a dent in the billion-dollar shortfalls the Commonwealth is facing. Behavioral finance is on his side, though how much of a difference it can make remains to be seen.

More from America’s Top States for Business:

How the trade war with China could crush California’s $2.7 trillion economy and hurt other states

A scorecard on the governors that want to beat Trump in 2020

These states are offering $10,000 or more to get you to live there

“The state budget is a big abstraction,” he says. “The sum of how Pennsylvania is doing is the sum of how Pennsylvanians are doing.”

Among his initiatives: $100 investment accounts for every baby born or adopted in Pennsylvania, a state-run automatic IRA to cover many of the 2.1 million people who don’t have access to a retirement plan, and big state tax breaks for people with disabilities.

Next up, he says, could be a program to automate claiming the earned income-tax credit — infamous for being so complex that 20% of eligible people don’t claim it.

Torsella has won support from such stellar corners as the Pew Charitable Trusts, but some people worry the growing role of government in encouraging savings will crowd out private-sector alternatives, reduce individual choice and potentially take the pressure off the federal government for real reform to basic government benefit programs.

The U.S. Chamber of Commerce says bare-bones state IRAs will cause small businesses to drop their 401(k) plans. The Investment Company Institute, which represents the mutual fund industry, opposes state auto IRA plans but supports national reform efforts. Currently, three states — California, Oregon and Illinois — have launched auto-IRAs. California launched its program on July 1.

“Recent efforts by state and local governments to place workers into government-run auto-IRA programs, however, are flawed in several ways. They are costly by comparison, and they effectively lack the protections of ERISA (Employee Retirement Income Security Act). Smaller employers in particular will be less likely to adopt more effective retirement savings plans — like Simple IRAs and 401(k) plans — instead falling back on the state- or city-mandated default IRA program,” it said in a statement.

Torsella says he’s not willing to wait for the federal government to act.

“I have zero patience for that criticism,” Torsella says. “As someone who wants to see broader changes to reform the system, I’m going to do, and we are going to do, what we can do.”

Despite other similar programs, Pennsylvania’s initiative stands out because of its size and swing-state status, and because Torsella keeps rolling out the initiatives. He says he wants to change Pennsylvanians’ financial health and help reconnect them to their communities.

Jump-starting a savings mentality

A longtime Democratic politician who also played a role in Philadelphia’s fiscal rebound in the 1990s and previously ran for the Senate, Torsella started on his savings trajectory after the success of the Treasury’s unclaimed property program, which enables people to search for accounts they’ve lost track of. (A surprising number of people, 1 in 10 in Pennsylvania, have lost track of accounts, such as orphan IRAs.)

The first day the Commonwealth enabled people to search its online portal, “we got a flurry of phone calls the next day,” Torsella says. “One was from a woman who ended up using the $2,500 she claimed to pay for cancer treatment she didn’t know she could afford.”

Torsella has taken that idea — that small amounts make a big difference in some people’s lives — and combined it with insights from behavioral finance.

This January, after a pilot program, Pennsylvania implemented the Keystone Scholars Program, a child savings plan that gives every baby $100 in an account managed by the state to be used for college. So far, about 2,700 people have taken the first step to claim the money. But they are not the first. Nevada and Rhode Island are each offering $100 grants, and Maine is offering $500.

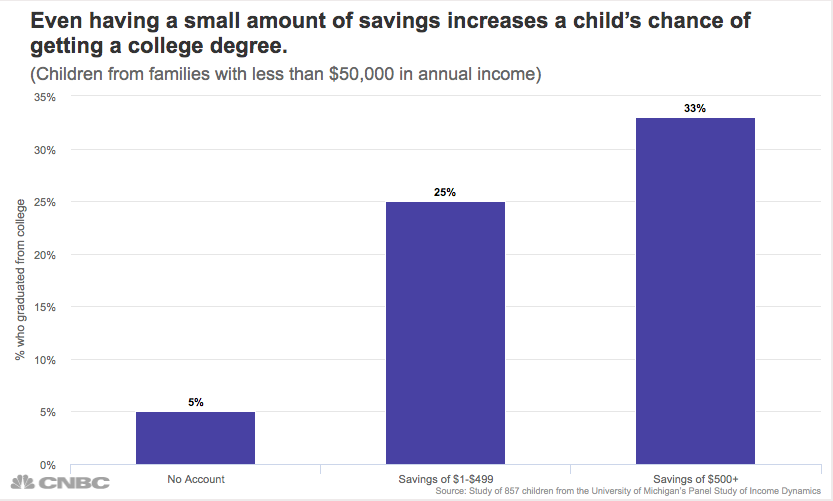

Research from Washington University in St. Louis shows that having any account at all increases the chances fourfold that a child from a low-income family will attend college. The theory is that people who feel the government has an interest in their success are motivated to push themselves.

Investment decisions and actual ownership reside with the state; the money plus returns will be available to the beneficiaries when they head to college.

One of the other possible benefits of the accounts is that they may spur more savings.

Philadelphia parents Harrison and Kaitlin Bradley opted in to the $100 account for their daughter, Miriam, at the same time they opened a Pennsylvania 529 account for their baby, born in April.

“To me it feels like the state cares about education,” says Kaitlin. “Now that we have a little one that’s headed to the school in the future, it makes me hopeful.”

There are 65 child savings programs across the country, covering 482,000 children, according to Shira Markoff, children’s savings director at Washington, D.C.-based nonprofit Prosperity Now.

Treasurer Torsella has exhibited unique leadership on retirement security by not just campaigning on the issue but following through with a task force and working with legislators on possible solutions.

John Scott

director of Pew’s retirement savings project

Among the states with child savings accounts, procedures to claim the money differ. Some, like Colorado and Pennsylvania, require the money be invested in a college savings plan. Some in the private sector, including well-known investment advisor Ric Edelman, have been pushing the idea of super-long-term savings accounts to take advantage of compounding over decades.

The government movement took off in 2011, when San Francisco started a program, but Pennsylvania’s move drew more attention, Markoff notes.

Torsella’s campaign for the auto IRA has been a longer one, in part because the program is more complicated, he says.

The idea behind state auto IRAs is that people have a harder time saving when they don’t have access to the convenience and discipline of automatic deductions of a workplace-based retirement plan. In Pennsylvania more than 500,000 people who lack access to a 401(k) work in companies with 50–499 employees, and another 703,000 work for businesses with 500 or more employees, according to a report by Torsella’s office.

He expects legislation to be introduced in the fall.

It would require employers (probably set at those with more than 10 employees) who don’t already offer a retirement plan to enroll their employees in the state-run plan. There also have been federal proposals, but none that have passed.

“Treasurer Torsella has exhibited unique leadership on retirement security by not just campaigning on the issue but following through with a task force and working with legislators on possible solutions,” said John Scott, director of Pew’s retirement savings project. “Even more remarkable is the fact that from the start he has included both political parties as well as labor and industry throughout the process.”

In April 2017, Torsella also helped create a savings account for people with disabilities, enabling them to save up to $15,000 a year, free of state taxes.

“We see this as an economic tapestry,” he says.

In a wider context, Torsella’s moves and those in other states and cities are part of a movement to reinvent government benefit programs, at least around the edges.

Treasurer of Pennsylvania Joe Torsella

Matt Rourke | AP

There used to be more of a consensus in the United States that one of the rights for citizens was a financial safety net. When it was enacted, Social Security was designed to make older Americans financially secure; today it replaces, on average, about 40% of a typical American’s income, though financial advisors typically recommend having 70%.

The idea that the government should provide broad grants for higher education also used to be more prevalent. By the time the original GI Bill ended on July 25, 1956, 7.8 million of 16 million World War II veterans had participated in an education or training program. More broadly, the proportion of federal grants to federal loans in 1976 was almost even, but by 1985 the ratio had shifted to 27% grants vs. 70% loans. By 1998 it shifted further, to 17% grants vs. 82% loans, according to research cited by William Elliott, associate professor at the University of Kansas.

Today 70% of students graduate with debt, and the average debt burden is more than $37,000. In 2005 it was about $20,000.

Financial insecurity is one of the roots of the sense of disconnect people feel to their communities today, Torsella says.

“If you can break through the myth that savings is only for rich people with financial advisors, you can begin to create a virtuous circle rather than a viscous cycle,” says Torsella. “Financial literacy is threaded through the income and wealth gaps we have. “